Table of Contents

Explore this article with AI

Has a property recently been left to you in a will, and you’re unsure what to do next? Inheriting real estate can feel overwhelming; especially during an already emotional time. This comprehensive guide will help you understand every step of the process so you can make the most of your inherited home or investment property.

As a local team that specializes award-winning property management in Orange County, CA, we know firsthand the mix of challenges and opportunities that come with inheriting real estate. For more than 15 years, we’ve helped homeowners and families across Irvine, Anaheim, Huntington Beach, and the greater Orange County area, navigate the complexities of inherited properties. Whether you’re thinking about selling, renting, or keeping the property, our article will cover everything you need.

Disclaimer: We are not certified public accountants, estate planners, or attorneys. You should consult qualified professionals for legal, tax, or estate planning advice related to an inherited property.

What Are My Options When I Inherit a House?

Inheriting a home comes with new financial and legal responsibilities. Once ownership officially transfers to you, you typically have three main options to consider.

1. Move Into the Home

If the inherited property is in good condition and fits your lifestyle, you might decide to make it your personal residence. Living in an inherited home can be a meaningful way to preserve family memories or enjoy a desirable neighborhood.

One major advantage is that inherited homes receive a stepped-up basis. This means that the property’s value resets to its fair market value at the time of inheritance. This can help reduce future capital gains taxes if you decide to sell later.

However, once you take ownership, you’ll also take on ongoing expenses such as property taxes, insurance, utilities, and regular maintenance. Before moving in, it’s smart to review your budget, schedule an inspection, and make sure keeping the property makes financial sense for your long-term plans.

2. Rent the Property

Turning your inherited home into a rental can be a great way to generate consistent income while keeping the property in your family. California’s rental market (especially in areas like San Diego, Orange County, and the Bay Area) remains strong, which could make the property a potentially rewarding investment.

That said, being a landlord involves ongoing responsibilities, from finding qualified tenants to handling maintenance, repairs, and compliance with local rental regulations. Many heirs choose to partner with a professional property management company like Good Life Property Management, which can take care of everything from marketing and tenant screening to rent collection and maintenance coordination. With expert help, your inherited property can become a reliable source of income without the stress of day-to-day management.

3. Sell the Property

If the inherited home doesn’t fit your needs, or if you’re sharing ownership with other heirs, selling may be the best choice. Selling allows you to unlock the property’s cash value, simplify your finances, or divide proceeds fairly among family members.

The good news: most heirs pay little or no capital gains tax when selling shortly after inheritance, thanks to the stepped-up basis that adjusts the property’s taxable value to its current market price. Before listing, schedule an appraisal, take care of any necessary repairs, and consult a real estate or property management professional to help you maximize your return.

Additional Factors to Consider

When you inherit a home in California, it’s important to consider a few additional details before making major decisions:

- Taxes: California does NOT have a state inheritance tax, but federal estate taxes may apply to very high-value estates.

- Mortgages: If the property still has a mortgage, you or the estate must continue payments or refinance it into your name. For reverse mortgages, repayment is typically required within six months of the borrower’s passing.

- Property evaluation: Scheduling an inspection and appraisal early will help you understand the home’s condition, establish your tax basis, and guide decisions about repairs, insurance, and long-term planning.

What Is the First Thing You Should Do When You Inherit a House?

Inheriting a home can be both emotional and overwhelming. Along with sentimental value, it often comes with important financial and legal responsibilities. Whether the property is paid off, has a mortgage, or includes a reverse mortgage, taking the right steps early can help you protect your new asset and avoid costly mistakes.

Here’s where to start:

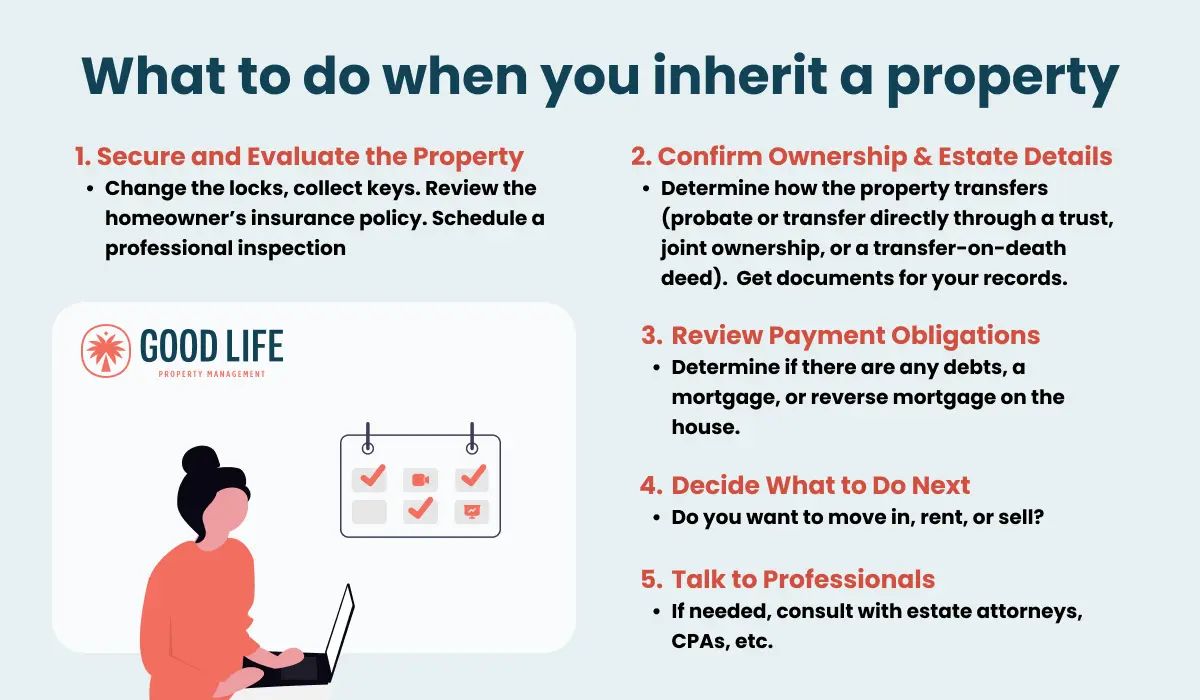

1. Secure and Evaluate the Property

- Secure the home: Change the locks, collect any spare keys, and make sure the property is protected.

- Check insurance coverage: Contact the insurance provider right away. Many homeowners policies lapse after the original owner’s passing, leaving the property uninsured.

- Schedule an inspection and appraisal: This will help you understand the property’s current condition and market value.

2. Confirm Ownership and Estate Details

- Determine how the property transfers: In California, a home may pass through probate or transfer directly through a trust, joint ownership, or a transfer-on-death deed.

- Verify your authority to act: Obtain a copy of the will, trust documents, or court-issued letters testamentary/administration if probate is required.

- Understand the probate process: California probate can take several months, so confirming your role and legal rights early is key to preventing delays.

3. Review Financial Obligations

- Identify any debts: Check for mortgages, liens, unpaid property taxes, or HOA dues.

- If there’s a mortgage: Contact the lender immediately to discuss your options for assuming, refinancing, or paying off the loan.

- If there’s a reverse mortgage: Notify the lender and confirm repayment deadlines (typically six months from the borrower’s passing).

4. Decide What to Do With the Property

You typically have three main options:

- Live in it: Make the property your new home.

- Rent it out: Turn it into a long-term investment and enjoy steady income.

- Sell it: Liquidate the asset. Thanks to the stepped-up basis rule, you may owe little or no capital gains tax if sold soon after inheritance.

At Good Life Property Management – Orange County, we’ve helped homeowners across California navigate these choices with confidence. From assessing rental potential and coordinating repairs to handling tenant placement and full-service management, our team can help you make the most of your inherited property, without the stress.

5. Consult Professional Advisors

Before making major decisions, it’s smart to talk with:

- A CPA or tax advisor about inheritance and capital gains implications.

- An estate or probate attorney to confirm ownership and transfer details.

- A property management professional (like Good Life) for guidance on rental, maintenance, or sale options.

What Happens When You Inherit a House That’s Paid Off?

If you inherit a property that’s already paid off, you’re in a fortunate position, then the home transfers to you free of debt once probate (if required) is completed. You’ll own it outright with no remaining mortgage to worry about.

What You’ll Need to Do:

- Update the deed to reflect your ownership.

- Keep up with ongoing expenses like property taxes, insurance, and maintenance.

- Decide whether to live in, rent out, or sell the property.

California Note: Once title officially transfers, the home generally becomes your separate property (even if you’re married), unless you choose to commingle it with community assets or funds.

What Happens When You Inherit a House With a Mortgage?

If the home still has an active mortgage, you inherit both the property and its financial obligation. While many loans include a due-on-sale clause, the Garn–St. Germain Depository Institutions Act prevents lenders from demanding full repayment immediately after inheritance. This means you can usually assume the existing loan or refinance it in your own name.

Your Options:

- Keep the loan: Continue making payments if you plan to keep or rent the home.

- Refinance or sell: If the payments don’t fit your budget, refinance for better terms or sell the property to pay off the balance.

Important: Until probate is finalized and title is transferred, the estate remains responsible for making mortgage payments to avoid default.

What Happens When You Inherit a House With a Reverse Mortgage?

A reverse mortgage works differently from a traditional loan. The original homeowner borrowed against their equity, and the loan becomes due once they pass away.

If you inherit a property with a reverse mortgage:

- The full loan balance must be repaid, typically within six months (though extensions are sometimes available).

- You have three main options:

- Pay off the loan: usually by refinancing it in your own name.

- Sell the home to cover the balance; if it sells for more than what’s owed, you keep the difference.

- Deed the property to the lender if the mortgage exceeds the home’s value.

California Note: While heirs generally gain the right to the property upon inheritance, the reverse mortgage must be settled before ownership can be fully claimed or transferred.

How Does Inheriting a House Affect My Taxes?

One of the most common questions people have after inheriting real estate is how taxes will apply. The good news: in most cases, you won’t owe any taxes right away just for inheriting a property. However, it’s important to understand how estate taxes, property taxes, and capital gains may affect you later; especially if you decide to sell or rent the home.

1. Federal and California Estate Taxes

When someone passes away, any applicable estate taxes are paid by the estate before assets are distributed to heirs, not by you personally.

Federal Estate Tax:

- Applies only to estates valued above $13.99 million (as of 2025), meaning most families are fully exempt.

- If the estate exceeds that threshold, taxes are paid from the estate before inheritance transfers.

California Estate Tax:

- California does not impose a state estate or inheritance tax, so you won’t owe any state-level taxes just for inheriting property.

- Only federal estate tax rules apply, depending on the total estate value.

You can learn more about estate tax thresholds from the IRS Estate Tax page.

2. Property Taxes

Once the property transfers to you, you’ll take over annual property tax payments based on the home’s assessed value.

In California, Proposition 13 limits annual increases in assessed value to 2%, but reassessment may occur when ownership changes, including through inheritance. However, Proposition 19 allows some parent-to-child (or grandparent-to-grandchild) transfers to avoid reassessment if certain conditions are met.

Key Points:

- Property taxes are typically 1% of the home’s assessed value, plus local taxes or assessments.

- Payments are due twice per year (November 1 and February 1) and considered delinquent if unpaid after December 10 and April 10.

- You can find your local tax rate through your County Assessor’s Office.

3. Capital Gains Taxes (When You Sell)

If you sell the inherited home, you might owe capital gains tax, but often very little, thanks to the stepped-up basis rule.

Stepped-Up Basis Explained:

When you inherit a property, its tax basis (the amount used to calculate gains or losses) resets to its fair market value on the date of death.

Example:

If your parent purchased the home for $200,000 and it’s worth $800,000 when you inherit it, your new tax basis is $800,000.

If you sell soon after for $810,000, your taxable gain is only $10,000 — not $610,000.

Primary Residence Exemption:

If you move into the home and live there for at least two years, you may qualify for the $250,000 (single) or $500,000 (married) capital gains exclusion when you sell.

Reference: Learn more from the IRS Capital Gains Tax Guide.

4. Rental Income and Taxes

If you decide to rent out your inherited home, you’ll need to report the rental income on your annual tax return. The good news: you can also deduct a variety of expenses, including:

- Repairs and maintenance

- Property management fees

- Insurance and property taxes

- Depreciation

- Mortgage interest (if applicable)

5. Estate Administration and Other Costs

In some cases, the estate will still need to handle final tax obligations before transferring ownership:

- The executor may need to file a final income tax return for the deceased.

- The estate may require an EIN (Employer Identification Number) from the IRS for any income earned before distribution.

- Any income generated by the estate (such as rent collected before transfer) must be reported on an estate income tax return (Form 1041).

Bottom Line

Inheriting a home in California rarely triggers immediate taxes, but your future tax liability will depend on what you choose to do with the property. Whether you plan to sell, rent, or move in, consulting a qualified CPA or estate attorney early on can help you make smart, tax-efficient decisions.

How Good Life Property Management Can Help

At Good Life Property Management, we’ve helped countless California homeowners make informed, confident decisions about inherited real estate. Our goal is to help you protect your new asset, minimize stress, and maximize your financial return; no matter what path you choose.

Whether you’re planning to rent your inherited home, sell it, or explore both options, our experienced team will guide you through every step of the process.

Schedule a free consultation today to discover how Good Life can turn your inherited property into a smooth, successful investment.

Our Blogs

24 Holiday Activities to do in Orange County

Discover the best Orange County holiday activities for 2025, including boat parades, theme park celebrations, waterfront light displays, and more.

Should I Buy a Home Warranty for My Rental Property?

When talking about rental properties, home warranties aren’t a good idea. But why? We’re sharing 4 reasons rental properties don’t mesh with home warranties.

Understanding Rent Control in Orange County, California

We’re breaking down the basics of rent control in Orange County, and exploring what the rent control laws mean for landlords and tenants.